What role do equities play in Troy’s Multi-Asset strategy?

The function of economic forecasting is to make astrology look respectable.

– John Kenneth Galbraith

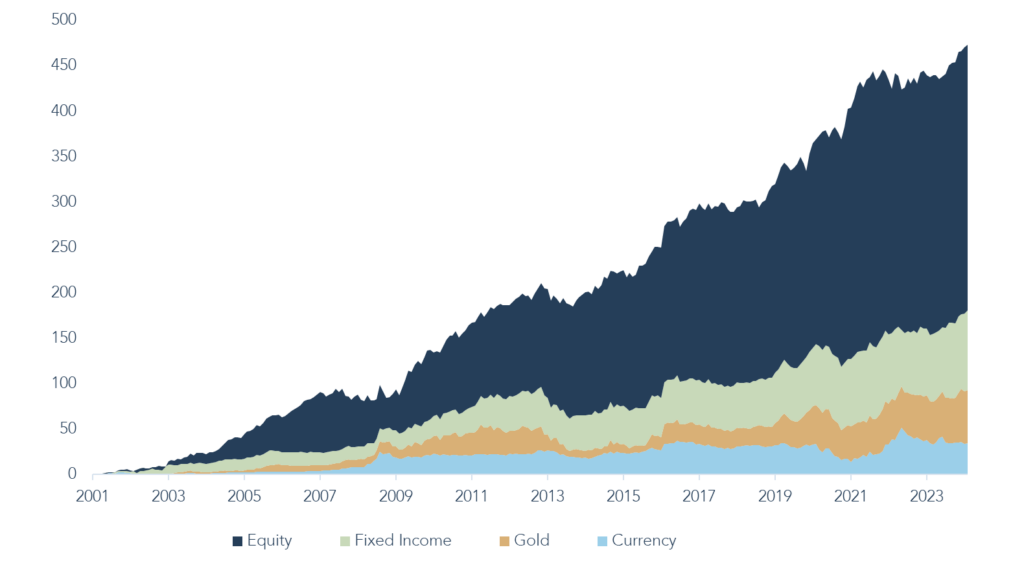

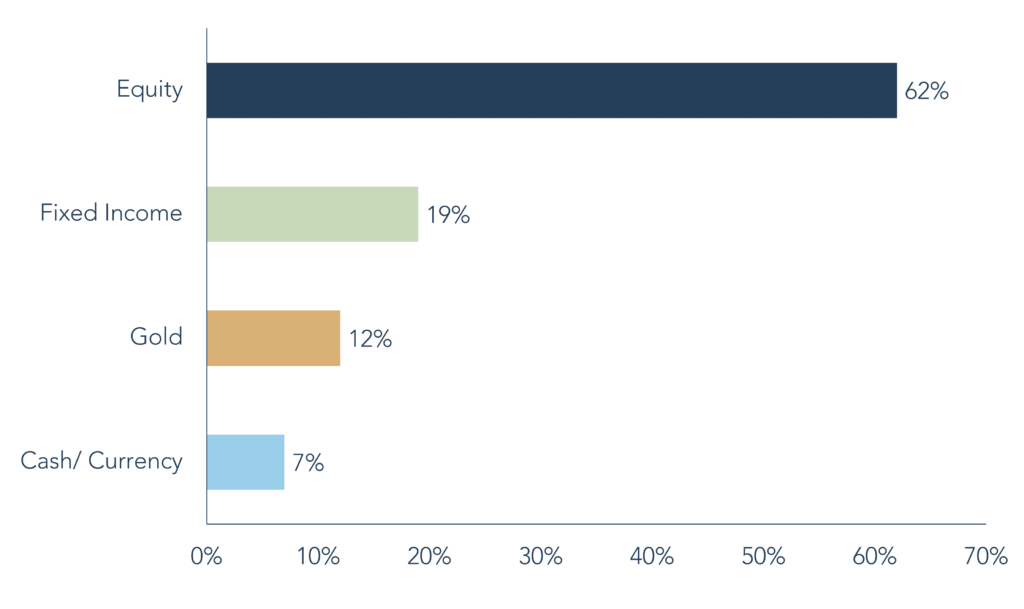

Troy’s Multi-Asset Strategy seeks to protect our investors’ capital and increase its value over the long term. Whilst the first part of this equation warrants some diversification by asset class, equities have proven to be by far the most effective way of growing capital above inflation over the long run. Since its inception in 2001, equities have driven approximately two thirds of the strategy’s returns. They are likely to continue to do much of the heavy lifting in the future. As a result, equities form the backbone of Troy’s Multi-Asset Strategy and the basis of the strategy’s dynamic asset allocation. As equity valuations fall, you should expect us to increase the strategy’s equity exposure. Conversely, as they rise, we will become increasingly conservative.

An equity-first mindset provides clarity to our approach that stands in stark contrast to other multi-asset investors. Whereas others will view equities as just one lever among many, for us it forms a central point of control. Our approach reduces errors in execution that can multiply as the number of investments increases. The greater the number of moving parts, the harder a portfolio is to manage, especially as correlations between different assets tend to break down at inopportune times.

At Troy, we take a strategic and long-term view, allocating capital to equities, fixed income, gold and cash (‘liquidity’). We strive to strike a sensible balance between risk and return, aiming to limit drawdowns but retaining the potential to participate in the upside. Having an equity-focused approach to asset allocation introduces some sensitivity to general equity markets but ensures we never lose sight of what drives long-term returns. Aligning ourselves with the success of high-quality companies has enabled us to generate returns without constantly needing to be right about the macro. Simply put, using equities as a guiding light has been the best way to navigate the vicissitudes of dynamically changing markets, and deliver on our dual mandate of preserving our clients’ hard-earned capital and growing it in real terms over time.

Long term drivers of returns by asset class

Return contribution since launch

Source: FactSet, 30 June 2024. Past performance is not a guide to future performance. Asset allocation subject to change. Contribution to return is gross of fees. Fees will have the effect of reducing performance. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-Asset Strategy.

What do we look for in equity investments?

The greatest long-range investment profits are never obtained by investing in marginal companies. – Phil Fisher

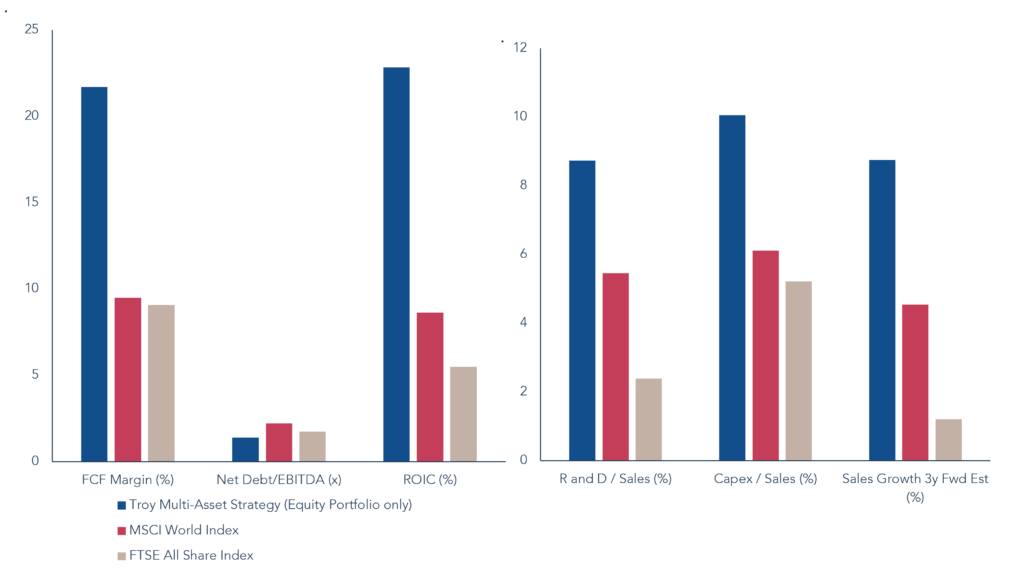

Our equity selection can be described as defensive, but it would be an error to see our approach as an extension of our macroeconomic views. Companies are selected on their individual merits to deliver attractive returns over the long term. This perspective is informed by an appreciation of where equity losses tend to occur. We believe the best way to both preserve and grow our clients’ capital is to combine a focus on investing in exceptional companies that can grow at sustainably high returns, with an emphasis on minimising the operational, financial and valuation risks that frequently lead to permanent impairments of capital.

The companies we invest in are anti-fragile 1 in nature and can sustain a high return on capital owing to identifiable competitive advantages. They are highly profitable and have robust finances due to strong cash generation and sturdy balance sheets, making them resilient during difficult economic environments and allowing them to reinvest in their businesses for future growth. We favour dependability over novelty, preferring large and established businesses with a track record of success to younger and less mature ones. We seek companies with consistent and predictable revenues and earnings, whilst avoiding those that are capital intensive, overly exposed to the vagaries of an economic cycle, or require significant leverage to generate respectable returns. For instance, we have long-standing holdings in consumer staples such as Nestlé and Procter & Gamble, but do not invest in airlines, banks, real estate, housebuilders, or other industries with a track record of raising capital and diluting shareholders at the worst possible times. Nor do we typically invest in commodity or energy companies, where success is predicated on extrinsic factors outside of a company’s control.

Resilient Quality & Adaptable Growth

Source: FactSet and Troy Asset Management Limited, 31 August 2024. Past performance is not a guide to future performance. Characteristics are shown excluding banks. Free Cash Flow measures are based on trailing figures over the last 12 months. Asset allocation subject to change. Estimates may not be achieved. All references to benchmarks are for comparative purposes only. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-Asset Strategy.

We focus on the durability of a company’s growth rather than the pace of it. Fast-growing companies can stir investor emotions, leading to elevated valuation risk, whilst also attracting greater competition. Businesses that persistently grow at steady rates over long periods of time are often undervalued by the market. Experian, another portfolio holding, provides a good example. Never the fastest grower, Experian’s steady growth through the cycle, underpinned by the strength of its credit data, has allowed Experian’s shares to compound at just over 13% since coming to market in 2006.

Companies are living, breathing organisms. The average lifespan of a company in the S&P500 is a little over 21 years.2 Delaying the inexorable march of entropy requires far-sightedness, an advantaged business, and good operational execution. As long-term investors, we want the companies in which we invest to be managed and governed by capable and trustworthy people who are closely aligned with shareholders. In management we seek stability and consistency of strategy, as well as an incentivisation structure that encourages disciplined capital allocation and promotes the sustainable delivery of shareholder value over the long run. By contrast, we look to avoid hired guns who prioritise their own short-term interests. American Express’ actions during the pandemic are illustrative of the long-term approach we value. Despite severe disruption, American Express did not lay-off staff, but instead reinvested in its business to improve the value of its offering. The result has been accelerating revenue growth and significant success among a younger cohort of Generation Z and Millennial consumers.

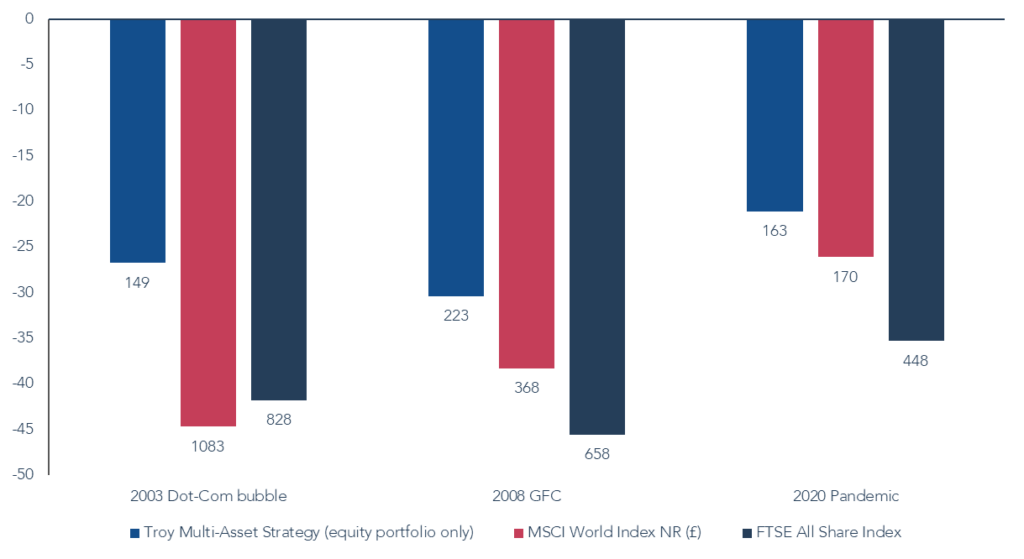

Valuation is important because overpaying is another risk to prospective returns that we seek to minimise. A quality company may not make a great investment if bought expensively. Over the Multi-Asset Strategy’s life, we have always patiently waited for the right opportunity before investing. For instance, Visa has been long admired but the holding was built in the early stages of 2020 when the pandemic created an opportunity to invest at temporarily depressed prices. This valuation discipline has served us well, allowing us to avoid extreme share price moves during periods of dislocation and capture the underlying compounding of our companies’ operational performance over the long term. An overarching focus on quality, combined with a strong valuation discipline, has resulted in the equity portion of the portfolio suffering less significant drawdowns, and then recovering faster, than broader equity markets during periods of dislocation. In turn, this has supported the Strategy’s objective of protecting capital on the downside and delivering strong risk-adjusted returns.

Maximum Drawdown (%) and Days Recovery

Source: FactSet, since launch 31 May 2001 to 30 June 2024. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-Asset Strategy.

What is our investment edge?

The stock market is a device to transfer money from the impatient to the patient’.

– Warren Buffett

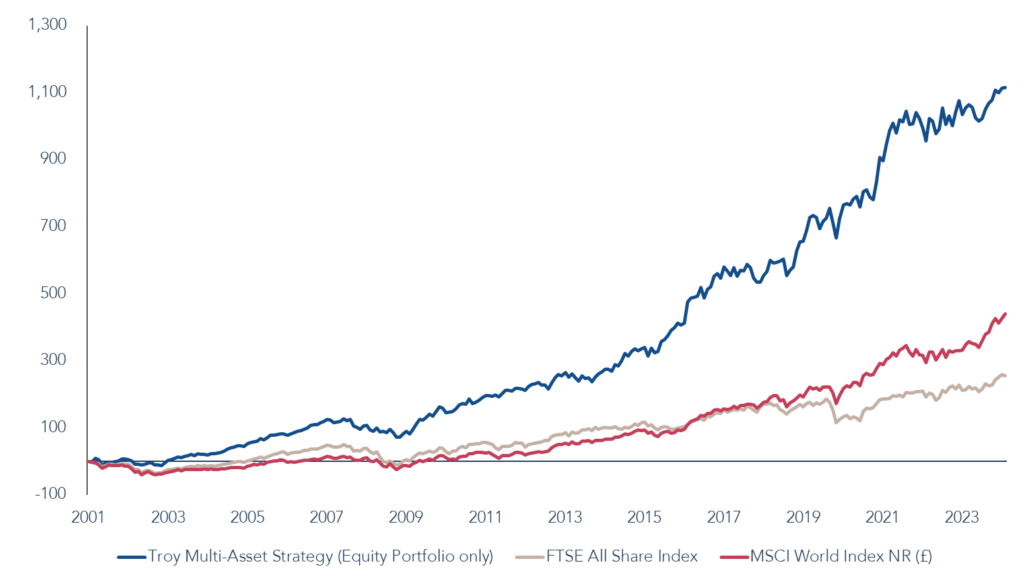

Since its launch in 2001, the equity portion of the Multi-Asset Strategy has significantly outperformed global equity markets. We believe we have several advantages, both structural and behavioural in nature, that should help sustain success in the future.

Troy Multi-Asset Strategy (Equity-Only) Vs The FTSE All-Share Index And MSCI World Index (%)

Source: Troy Asset Management Limited, 30 June 2024. Neither actual nor simulated past performance results are guides to future performance. Simulated gross performance is for illustrative purposes only and is not representative of how Troy would construct the portfolio. All references to benchmarks are for comparative purposes only. The simulation is based on the equity component of Troy Multi-Asset Strategy. Performance has been calculated based on the equity holdings over the period representing 100% of the portfolio, however equity exposure over the period has varied significantly depending on the Manager’s views at the time. As a multi-asset strategy, the portfolio has been invested in other asset classes which contribute to the overall returns. The returns of any overseas equities will also be impacted by the currency movements over the period.

We believe markets persistently underestimate the longevity and compounding power of those rare businesses that can grow at sustainably high rates of return over time. This is unsurprising given that most companies see their returns quickly competed away, lack a large enough addressable market to sustain attractive levels of growth, or simply slowdown under the weight of their own success. This market inefficiency is likely to persist. Many market participants have short investment horizons, are impatient and prone to action, or simply lack the fortitude to hold on during difficult moments. At Troy, our holding periods are deliberately long to exploit this time arbitrage. We do thorough research and develop a deep understanding of the companies we invest in, allowing us to remain constant in our conviction when equity markets are volatile.

Troy can invest with patience because there is a close alignment between all stakeholders in our business. Private ownership, with equity widely owned by Troy’s employees, results in a shareholder base that is closely aligned with our long-term investment objectives. Troy is not distracted by outside pressures and can steer its own course.

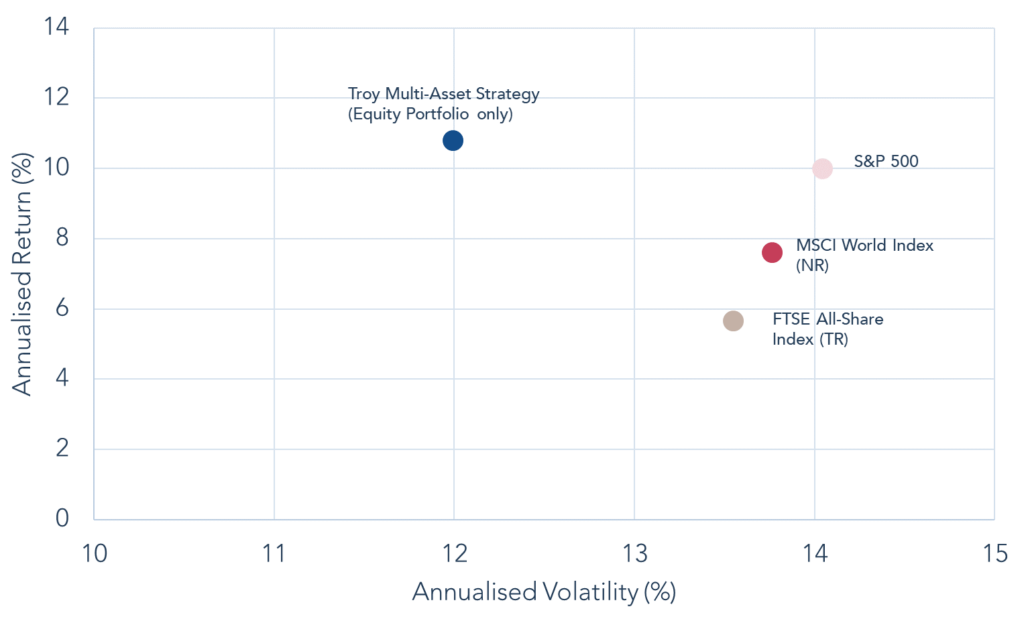

Risk/Return profile since inception

Source: FactSet, 30 June 2024, GBP gross of fees. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-Asset Strategy. The MSCI World is shown as a widely used global equity index.

We have always believed that attracting like-minded investors, who understand our investment philosophy, and focusing our efforts on meeting and exceeding their expectations is the best path to long-term success.

Source: Troy Asset Management Limited, 31 July 2024. Turnover is since inception, 31 May 2001 to 31 December 2023. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-Asset Strategy.

These structural underpinnings, as well as our focus on capital preservation, allow us to behave and invest in a markedly different way to many other equity investors. We care about absolute returns, not relative ones, and are not beholden to the composition of an equity index. We do not need to chase returns but can simply allocate to other asset classes should equity valuations become too rich, allowing us to be disciplined in waiting for attractive opportunities. This very different mindset affords us other behavioural advantages. It is well known that humans typically feel the pain of loss far more acutely than the joy delivered by investment gains. Significant declines in value can elicit visceral emotions that lead to irrational behaviour and the permanent loss of capital. The conservative nature of the Multi-Asset Strategy’s approach means that we naturally avoid these emotional extremes and continue to operate on an even keel. This allows us to be on the front-foot during periods of stock market stress and take advantage of low valuations that are created by the forced selling of others.

How do we sustain success?

Many of the advantages highlighted above are structural in nature and likely to persist. However, investing is highly competitive. To sustain good results, you must learn from your mistakes, recognise your biases, and strive to become a better investor over time.

By focusing on quality and trying to avoid the major pitfalls that lead to permanent loss of capital in equity investing, we have made more good investments than bad. Nevertheless, like all investors, we have made our fair share of mistakes along the way. One of our worst was early in the strategy’s life, when we invested in EMI. At the time, EMI was one of the dominant players in the music industry and traded on what appeared to be an attractive valuation. However, we underestimated the extent to which the industry was being disrupted as the consumption of music shifted online, undermining the economics of the large record labels. Whilst the investment was painful, the experience was a valuable one in highlighting that a cheap valuation is no protection against the dangers of being the wrong side of a secular trend.

Although we have made plenty of mistakes since then, we have become better at moving on from them faster. Henkel, a German company that sells home care and beauty products, as well as industrial adhesives, provides a good example. We were attracted by the potential of Henkel’s adhesives business, the company’s family ownership, and its strong track record and defensive profile. After initiating a holding in 2018 and getting to know management better, we quickly realised that Henkel was prioritising margins at the expense of reinvesting in its business. With this undermining our confidence in both Henkel’s management and the company’s long-term prospects, we quickly exited our holding at a similar level to our entry price. Six years later, Henkel’s shares trade significantly below the levels at which we sold.

An important element of successful investment is appreciating the behavioural biases associated with deep research and long holding periods. For instance, there is a risk that analytical objectivity decreases as familiarity grows, or that you become overconfident in your views of a company’s prospects. There is also the danger that familiarity breeds complacency, leading you to overlook the deteriorating performance of a struggling company, as well as ignore the opportunity cost of not owning something better.

We seek to manage and minimise these biases in a variety of ways. Whilst we have long holding periods, we believe that having some portfolio turnover is healthy. We want to own dynamic and thriving companies for the long run, not those in stasis or decline. There should be strong competition for capital within the portfolio, even if the barriers to entry are exceptionally high. We encourage rigorous discussion and debate by promoting a flat organisational structure where every member of the 14-strong investment team is expected to challenge assumptions and speak their mind. Each member of the team is a generalist, rather than specialist, which allows us to build broad knowledge and intelligently debate the relative merits of companies across very different industries and sectors. Expertise does not reside in the minds of one or two people but is broadly distributed across the team, helping to minimise individual biases and mistakes (this whitepaper provides a more detailed overview of how we collaborate as a team).

Our investment process includes several checks and balances that help ensure we do not rest on our laurels. For example, we formally review underperforming holdings on a regular basis, including critically debating the merits of companies that have either suffered sharp share price declines or delivered underwhelming performance over a prolonged period. Additionally, we have quarterly risk and investment oversight meetings, where we systematically review performance, the efficacy of our decision making and the changing operational, financial and valuation risks of the companies we own. Moreover, we hold regular research lunches throughout the year, as well as an investment team offsite, to continuously assess how we can incrementally improve as investors.

How do we weight equities in the portfolio?

You make most of your money in a bear market, you just don’t realise it at the time

– Shelby Cullom Davis

Our asset allocation is flexible in nature. Since its inception in 2001, the Multi-Asset Strategy’s equity allocation has ranged from as low as 20% to as high as 72%, reflecting the dynamism of our approach. A belief in the compounding power of high-quality equities means we are unlikely to ever have a weighting of less than 20% in equities. Similarly, given our focus on capital preservation, a weighting as high as 72% will not be sustained for any great length of time. On average, the strategy’s equity exposure has been 40%, illustrating the general balance we strike between growing our investors’ capital and not exposing them to extreme equity market drawdowns. We will often be early in taking risk off the table, given that market exuberance can last longer than expected, but are compensated for our caution when sell-offs arrive.

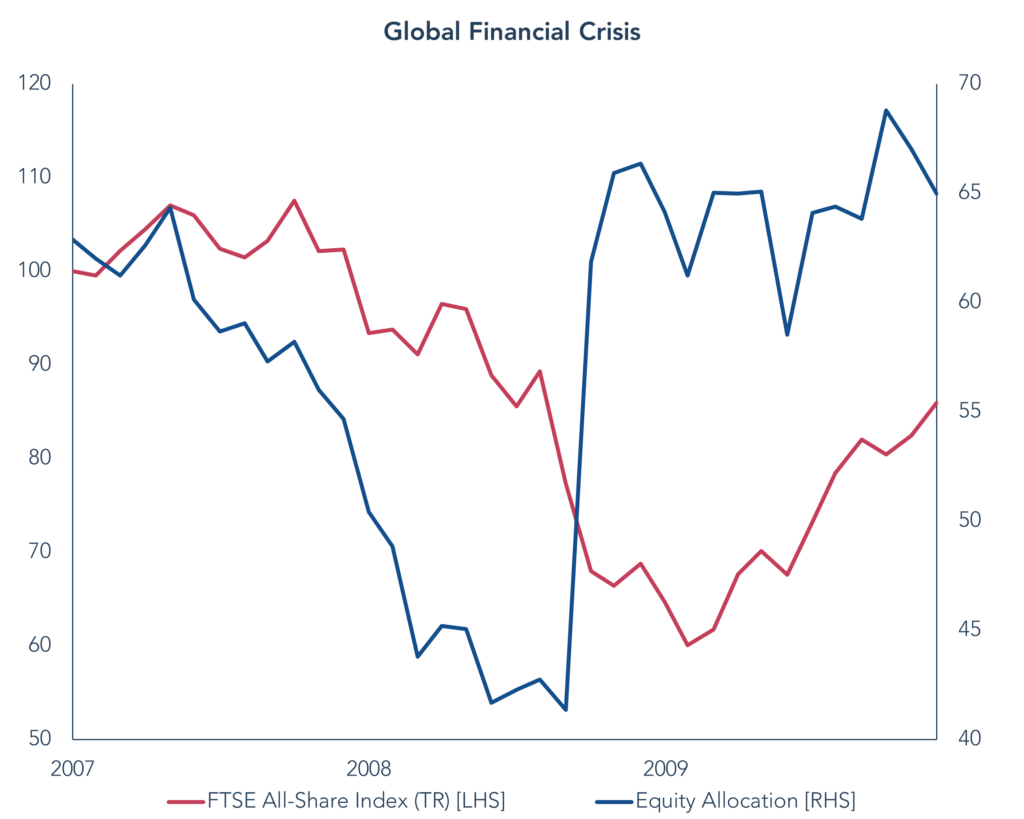

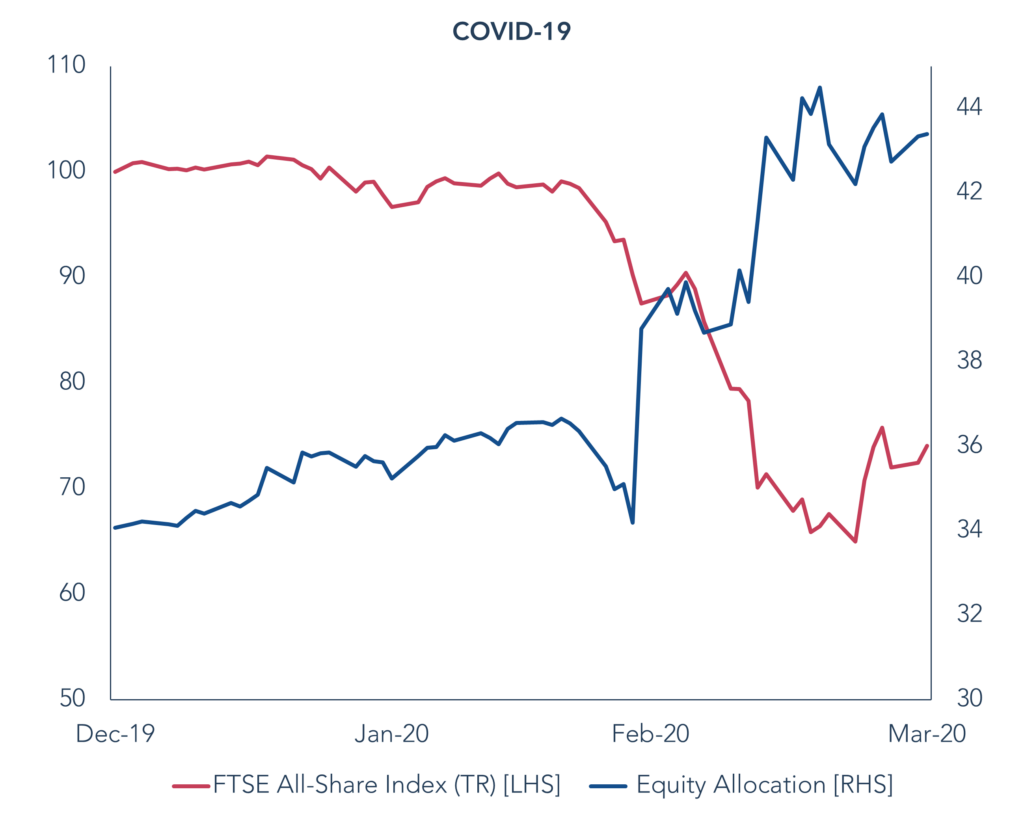

The strategy’s equity weighting is determined by the interplay between the valuations of the equities we favour, the relative attractiveness of other asset classes and the broader macroeconomic backdrop. By way of example, the equity weighting significantly increased during the global financial crisis. Despite a high level of macroeconomic uncertainty, equity valuations dropped to generationally low levels, giving us confidence of accessing strong prospective returns. Conversely, a lower-than-average equity weighting since 2021 reflects relatively rich equity valuations, a higher cost of capital, stickier inflation and growing geopolitical tensions. It is also the result of the attractive real yields on offer in short-dated US Treasury Inflation-Protected Securities (TIPS), which are at their highest levels since 2009 (explored in more detail in this note). Even during periods when the strategy’s equity weighting is relatively low, we are always alert and guided by the idiosyncratic opportunities our research uncovers.

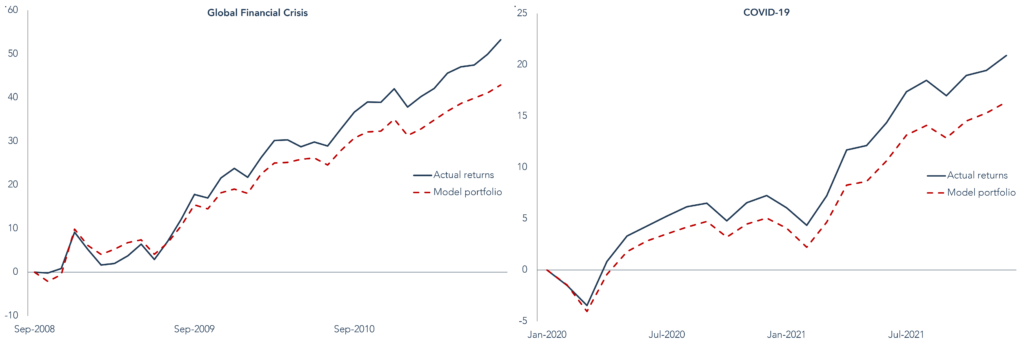

Dynamic Asset Allocation During Market Drawdowns

Source: Troy Asset Management Limited, 30 June 2024. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Asset Allocation and holdings subject to change. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-Asset Strategy.

Although the strategy’s asset allocation typically evolves slowly over time, it can change rapidly when opportunities abound. The ability to be dynamic and move quickly has significantly improved the strategy’s risk-adjusted returns. Since its inception in 2001, the strategy has faced numerous major market events, including the bursting of a technology bubble, a global financial crisis, and more recently a pandemic. Despite the very different nature of each of these crises, the strategy’s behaviour has been consistent. We have protected capital well on the downside but also added to our equity exposure at depressed prices, increasing our participation on the upside as equity markets recover.

Simulated performance comparing portfolio returns vs static portfolio during market drawdowns

Source: Troy Asset Management Limited, 30 June 2024. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Asset Allocation and holdings subject to change. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-Asset Strategy.

Summary

Having equities as the North Star for our asset allocation, provides a simple clarity to our approach. We are not constantly trying to decipher an inherently uncertain future. Instead, we place our faith in high-quality competitively advantaged companies that are resilient, adaptable and able to flourish in an ever-changing world. We invest in these companies for the long run, allowing them to compound shareholder value and do the heavy lifting for our returns.

We dial the strategy’s equity weighting up and down based on the opportunity set. We are cautious when risks are elevated and dynamically increase our equity exposure when opportunities are plentiful. In doing so, we look to exploit persistent behavioural advantages. We are not bound to an equity index or under pressure to chase equity returns. We can be patient and disciplined, exploiting the irrational behaviour of others during turbulent times. By investing counter-cyclically, we have protected our investors from a rollercoaster of emotions and provided them with a smoother and more comfortable ride. As importantly, by defending capital on the downside and recovering losses quickly, we have delivered strong risk-adjusted returns over the long term.

1Antifragility is a concept developed by Nassim Taleb, which describes the ability to not only withstand stress and adversity but thrive under such conditions.

2https://www.statista.com/statistics/

Please refer to Troy’s Glossary of investment terms here. The information shown relates to a mandate which is representative of, and has been managed in accordance with, Troy Asset Management Limited’s Multi-Asset Strategy. This information is not intended as an invitation or an inducement to invest in the shares of the relevant fund. Performance data provided is either calculated as net or gross of fees as specified in the relevant slide. Fees will have the effect of reducing performance. Past performance is not a guide to future performance. All references to benchmarks are for comparative purposes only. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. There is no guarantee that the strategy will achieve its objective. The investment policy and process may not be suitable for all investors. If you are in any doubt about whether investment policy and process is suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party. Although Troy’s information providers, including without limitation, MSCI ESG Research LLC and its affiliates (the “ESG Parties”), obtain information from sources they consider reliable, none of the ESG Parties warrants or guarantees the originality, accuracy and/or completeness of any data herein. None of the ESG Parties makes any express or implied warranties of any kind, and the ESG Parties hereby expressly disclaim all warranties of merchantability and fitness for a particular purpose, with respect to any data herein. None of the ESG Parties shall have any liability for any errors or omissions in connection with any data herein. Further, without limiting any of the foregoing, in no event shall any of the ESG Parties have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. Issued by Troy Asset Management Limited, 33 Davies Street, London W1K 4BP (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP. Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training. Any fund described in this document is neither available nor offered in the USA or to U.S. Persons.

© Troy Asset Management Ltd 2024.